Cattle markets in Georgia remain at historically high levels. Both underlying market fundamentals – supply and demand – are contributing to the record-high cattle prices. Policy uncertainty affecting the supply side appears to be contributing most significantly to price volatility in the short run. However, the underlying supply factors are unlikely to change in the coming months. Demand for beef appears to be resilient but macroeconomic headwinds may create more significant consequences for the cattle sector.

Supplies remain tight with nearly all indicators pointing to lower inventories and production. Cattle on feed, cattle slaughter, and beef production have all been below year-ago levels. The one area of strength has been much higher carcass weights year-over-year.

Demand at the consumer level shows little signs of pulling back as beef prices remain well above last year’s price levels. Cutout values have shown relatively limited seasonal increases, but should rise through June.

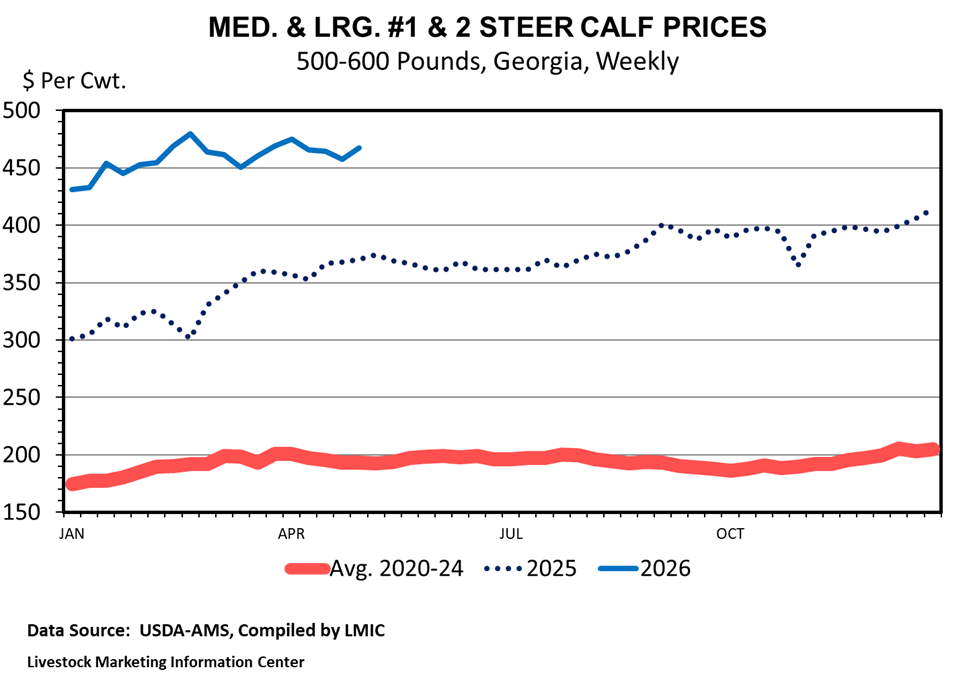

Combined, these tight supplies and robust demand have resulted in high fed and feeder cattle prices. Feeder cattle prices are also supported by relatively cheap feed. Feeder cattle prices in Georgia started the year higher and ramped up for several weeks (see Figure 1). Since early spring, prices have largely plateaued. Normal seasonal patterns would suggest that feeder cattle prices will continue to move sideways through the summer and drop off this fall. Cull cow prices are also up year-over-year but have shown a bit of weakness recently.

Uncertainty appears to be largest on the supply side in the form of beef import policy changes and the potential reopening of the Southern Border to Mexican feeder cattle imports. These are creating ‘headline’ risks that move markets in the short-run. However, significant fundamental supply factors of low inventories and production are unlikely to change for the next several months. More fundamental changes from demand may be more worrisome. Consumers are facing higher inflation, and some indicators point to weakening consumer finances. These demand factors are faster to change than supplies, but even so, these would likely materialize over a few months, not days or weeks.

While the general cattle outlook for the remainder of 2026 is for cattle prices to remain elevated, risks are always important to watch when making marketing and planning decisions.